Reserve Bank of India brought Emandate into force on 1 October 2021.

As we saw in RBI Emandate: Revenue Killer Or Consumer Interest Savior?, this regulation impacts recurring payments and auto debits (“Standing Instructions”) set up with credit card and debit card.

This was after a postponement of six 24* months at the behest of banks who sought more time to implement the changes to their systems called for by the new regulation. (* According to an RBI honcho interviewed in a podcast, Emandate was originally slated to go live on 30 September 2019.)

As I highlighted in my previous blog post, all hell broke loose after Emandate went live.

Perfectly legitimate payments have been getting declined since the beginning of October. It has also led to a sharp fall in the revenues of subscription economy companies.Perfectly legitimate payments have been getting declined since the beginning of October. It has also led to a sharp fall in the revenues of subscription economy companies.

While Emandate is overzealous, the fact is that the Indian banking regulator RBI had given enough time for banks and merchants to comply with it.

Ergo, all parties are equally to blame for the chaos currently prevailing in card-based recurring payments and auto debits.

Things are in a state of flux as of now but, if Positive Pay is any indication, it’s not hard to predict the trajectory of Emandate. (Spoiler Alert: Picture a pendulum swinging from one extreme to the other.)

Positive Pay.

Positive Pay.

If you can’t recall this expression, you’re not alone.

Announced in 2016, this regulation required payers who issued cheques above INR 50,000 ($667) to submit the details of the cheque to their bank in advance, failing which their cheques would be dishonored when they came for clearance.

The reg was meant to provide additional layer of security to cheques.

But my reflexive reaction was that Positive Pay is really Negative Pay – a new way for people and companies to delay payments and bounce cheques.

I've this feeling that "Positive Pay" will become another way of delaying payments à la "cheque is in the mail". pic.twitter.com/Mi0pUO573b

— GTM360 (@GTM360) June 8, 2016

It’s not that I’m against improving security for payments but I get mighty annoyed when regs treat security as an end in itself instead of the environment under which payments fulfill their raison d’être of enabling commerce.

I also felt that Positive Pay was a backdoor strategy to reduce cheque volumes and move payments to digital channels, especially the then nascent UPI.

Over the next few months, some of my banks announced that they had implemented Positive Pay and sent me emails to describe the steps required to log cheques above the ceiling. They also warned me that, if I failed to notify them in advance by following those steps, they’d bounce those cheques and slap me with NSF fees.

Some of my banks means not all of my banks.

I don’t recall hearing anything from State Bank of India, India’s largest bank and the only Fortune Global 500 bank out of India.

Subsequently, I’ve received several cheques in my company above ₹50,000 drawn on a variety of public sector and private sectors banks. All of them have cleared without any evidence that the payors had issued Positive Pay instructions to their banks.

I thought that the regulation was not applicable to cheques issued from business accounts.

Over the years, Positive Pay fell off my radar.

Then, a couple of weeks ago, I received a cheque drawn on an SBI personal account for an amount exceeding ₹50,000. I recalled Positive Pay and requested the payor to issue the necessary instruction to their bank so that the cheque wouldn’t bounce. They hadn’t heard about Positive Pay and did nothing. I deposited the cheque, bracing for it to return. But it cleared.

I was wondering how this was possible.

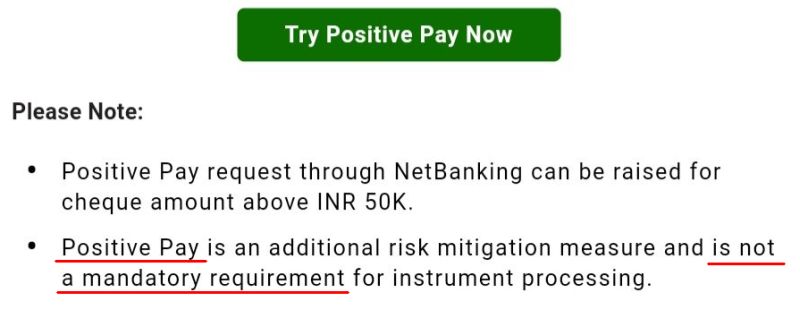

I went beneath the hood and found out that SBI has made Positive Pay optional. As a matter of fact, it has ignored RBI’s ₹50K figure and totally left it to customers to set their own caps beyond which they’d want Positive Pay to kick in. Click here for more details.

I went beneath the hood and found out that SBI has made Positive Pay optional. As a matter of fact, it has ignored RBI’s ₹50K figure and totally left it to customers to set their own caps beyond which they’d want Positive Pay to kick in. Click here for more details.

Kudos to SBI for getting that customers have varying risk profiles and transforming a “one size fits all” regulation into a highly customer-centric feature. Exactly what I’d expect from a brand for which I have cult loyalty.

I recently received an email from one of my other banks that had previously insisted on Positive Pay. As it says on the exhibit on the right, it has now made Positive Pay optional.

Ditto many other banks.

Dear sir/Madam, Positive pay facility is optional. However, Cheque Payments are now safer and more secure with Positive Pay System. Update key details of cheques issued for ₹50,000/- & above in Positive Pay, through I-net Banking & Go Mobile+ App.

— IDBI Bank Cares (@IDBIBankCares) October 22, 2021

In short, Positive Pay has fizzled out, thanks to the pushback from some large banks.

Emandate is not applicable to UPI standing instructions. Which is strange because, if enhancement of security were the only goal of the reg, UPI needs Emandate more than credit card since it’s irrevocable, has no fraud protection and touches my bank account directly – unlike my credit card.

IMO, by bringing only card-based standing instructions under its ambit, Emandate creates excess friction for card-based payments, and thereby diverts volumes to UPI through the backdoor. (Which is exactly what, as I noted earlier, I’d felt about Positive Pay when it was announced.)

I was once naive enough to believe that payment regulators would be unbiased about payment methods. Having outgrown that phase in my life, I’m okay with Emandate giving a biased boost to UPI.

1/2 Credit Card: Enter 3 digit CVV, wait for SMS, enter 6 digit OTP (more keystrokes if Card on File is banned).

UPI: Enter 4 digit static PIN.

I'm cool if the extra keystrokes are meant to divert payments from Credit Card to UPI.

— GTM360 (@GTM360) October 20, 2021

But I doubt if banks will be as blasé about this ploy as me.

Banks make interchange revenue on credit card and debit card payments. Whereas, ever since #ZeroMDR regulation came into effect from 1 January 2020, they earn zilch on UPI payments. As a result, they won’t be too happy about losing credit card and debit card volumes to UPI. Accordingly, I expect them to pushback on the new reg (As it is, they allegedly delayed it by 24 months.).

According to media reports, State Bank of India, India’s largest bank has not yet gone live with Emandate. I’m guessing that there’s more to SBI’s procrastination than meets the eye.

Going by what happened in the case of Positive Pay, if major banks pushback, Reg Emandate will fizzle out.

That would be a shame.

RegSM, as I’d termed the original remit of Emandate in Will Regulation Eliminate Subscription Trap? (Part 3), fulfills my lifelong dream for a payment workflow in which every charge to my credit card would need my separate approval.

Maybe it’s only me but I’m not a big fan of autodebits, and find very little difference between invisible payments and pickpocketing. I want my payments to be visible, especially when there are so many unscrupulous merchants out there.

Besides, RegSM will protect consumers from falling victims to subscription trap set by unscrupulous news, OTT and other Subscription Economy companies on their websites and app. As I’d observed back in April:

RBI’s new e-mandate rule will virtually kill Subscription Trap. It’s a great step to protect consumer interest – provided banks implement it via Opt Out. Kudos to RBI.

Accordingly, I think RegSM is a manna from heaven and don’t want it to fizzle out.

If the expansion of RegSM to Emandate is overzealous, so is the potential contraction of Emandate to nothing, just in the opposite direction. There’s a great need for nuance in such matters, as I highlighted in Don’t Throw The Baby Out With The Bathwater.

Ideally, Emandate should go back to its original RegSM remit where it covers only recurring payments for subscriptions (not autodebits for bill payments) and operates on the basis of opt-out (not opt-in).

Given below is my unsolicited suggestion for two alternative operating models for the revised Emandate / RegSM regulation:

MODEL 1

- Change from opt-in to opt-out.

- Remove the present ceiling of INR 5,000, and apply the reg on all recurring payments regardless of their value.

- Issuer bank should send an SMS informing about pending charge 24 hours in advance for all recurring payments.

- If customer wants to stop the charge, they reply STOP to the SMS and the bank declines the payment.

- If the charge is kosher, the customer does nothing, and the bank auto charges the credit card.

- If unscrupulous subscribers renege on subscriptions they’ve bought just because they can stop payments at will under this rule, merchants should be free to initiate action against them. More in How Merchants Will Thwart Subscription Dodgers (Part 4).

MODEL 2

- Banks list all credit card and debit card-based recurring payment mandates issued by their customers on their NetBanking portals.

- Customers can cancel the mandate on the bank portal anytime. In other words, they will not have to chase unscrupulous merchants to cancel their subscriptions.

In either model, everybody lives happily ever after. (UK has been using the second model for ages.)

If it’s recast according to either of these two models, I reckon that RBI Emandate will no longer be panned as revenue killer and start being celebrated as a savior of consumer interest.

Thank you RBI for helping me finally end my WSJ subscription.

— Sunil Nair (@spuriousmallu) October 4, 2021