I got my first credit card in 1988. I’ve been using credit card as my go-to method of payment since then. I also headed up the retail payments line of business at an old company. Safe to say that I’ve been tracking the credit card industry for close to four decades.

I’m fascinated by the massive boom in credit card in India in the recent past. The business in India has grown by 3X in the last five years. This growth is driven by an increase in the number of credit cards in circulation, rise in total payments value (TPV) processed with credit card, and many other factors.

In this blog post, I’ll unpack the explosive growth of the credit card business in India.

1. Credit Cards in Circulation

Credit card has been around in India for nearly 50 years (I got my first credit card in 1988, my father had one in 1976). In the first 45 years of the credit card industry until 2020, there were 40 million credit cards in India. In the following five years, the industry added 70 million new credit cards to hit a tally of 110 million credit cards in circulation by 2025 (Source). That’s a trebling in the count of credit cards in five years.

Put another way, the size of the credit card industry doubled in five years compared to the previous 45 years. These five years also saw massive growth of UPI volumes and value.

For the uninitiated, the split of credit cards in circulation in India across the various networks is as follows:

- Visa: 55M

- MasterCard: 40M

- RuPay: 15M

2. Credit Card Outstanding

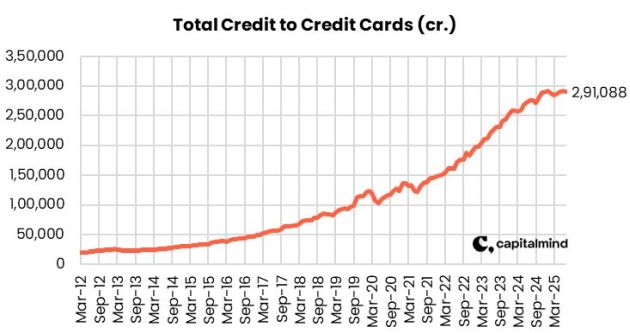

The TPV (Total Payments Value) of credit cards in India has jumped 3X in the last five years, as you can see from the following exhibit.

On a side note, it’s not just credit card. There has been an explosion in the volumes of other forms of consumer credit as well in India (see footnote 1).

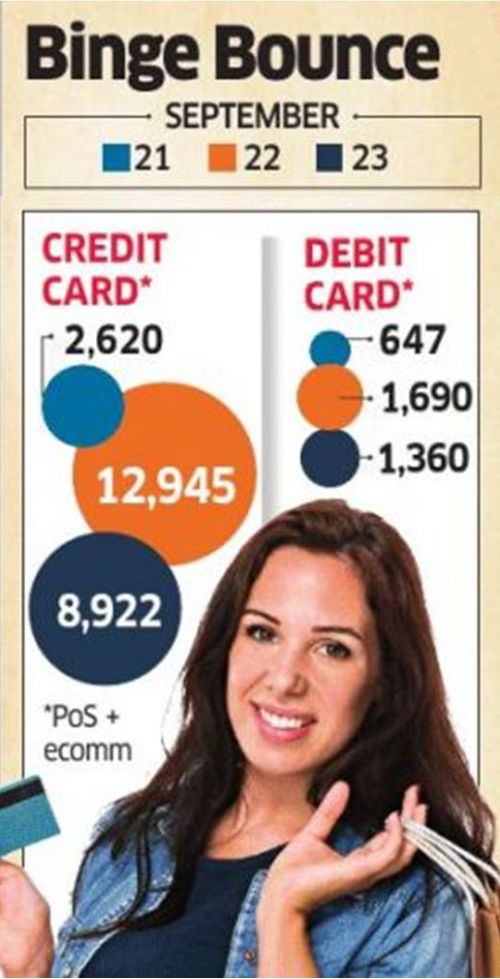

3. Credit Card Spike Caused By GST 2.0 Shopping

When the reduced GST rate regime came into effect in India on 22 September, there was a massive spurt in shopping between 21 and 22 September. This was reflected in the sharp jump in digital payments TPV between the two days. But all digital payments did not rise equally.

When the reduced GST rate regime came into effect in India on 22 September, there was a massive spurt in shopping between 21 and 22 September. This was reflected in the sharp jump in digital payments TPV between the two days. But all digital payments did not rise equally.

Credit Card TPV grew 395% from INR 2,620 crores / $308M to INR 12,945 crores / $1.52B, far outpacing the 37% growth in UPI TPV from INR 60,321 crores / $7.09B to INR 82,477 / $9.7B.

When UPI was launched in 2016, many people predicted that it would disrupt credit card. At the height of Kool Aid about the then newly launched A2A RTP method of payment, a government honcho predicted in 2017 that UPI would kill credit card by 2020. That did not happen.

Nine years later, it has still not happened.

In a follow-on post, I’ll advance some reasons why UPI has not disrupted credit card. Watch this space.

FOOTNOTE(S):

- Economic Times recently reported that Bajaj Finance “took 11 years to get to an AUM of INR 82,400 crores ($9.5 billion). In FY25 alone, it added INR 86,000 crore ($10.1 billion) to its AUM.” For the uninitiated, Bajaj Finance is the largest non bank financial corporation (NBFC) personal loan provider in India.