When you touch a hot plate, you’ll reflexively withdraw your hand and douse it in a bucket of ice to escape the hot burn. However, if you dunk your hand in ice without having touched a hot plate, you can get a frostbite.

When you touch a hot plate, you’ll reflexively withdraw your hand and douse it in a bucket of ice to escape the hot burn. However, if you dunk your hand in ice without having touched a hot plate, you can get a frostbite.

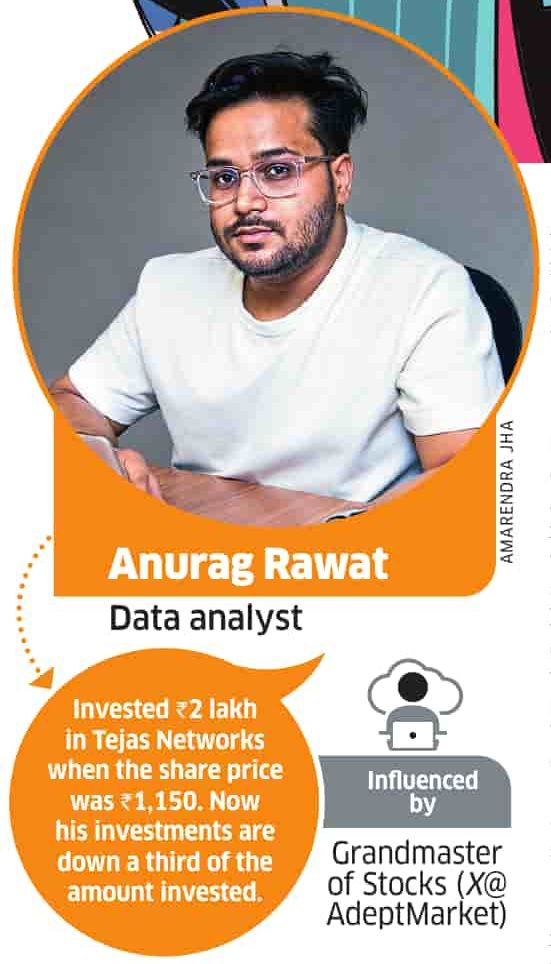

Likewise, a guy who bought a stock based on tips from a finfluencer and lost one third of his portfolio will reflexively swing towards fundamental analysis. However, that does mean that fundamental analysis is the panacea for all evils.

Firstly, fundamental analysis not feasible for everyone.

The average J6P can’t even read a PLBS. There’s no way he can DYOR (Do Your Own Research) since fundamental analysis of stocks requires tons of expertise. If he must get trained on fundamental analysis to acquire the required level of expertise, then he must dock the cost of the training course – they run into lakhs of rupees! – to his returns from his investments. If the net XIRR of their portfolio is then compared against fixed deposit or index fund, we might discover that a vast majority of retail investors lose money on direct equity investments (just as a SEBI study found that 89% of retail traders lose money on derivatives trading.)

Secondly, fundamental analysis is not necessarily valid in all situations. Take Bitcoin for instance. It defies all fundamentals but has delivered the highest returns of any asset class in history! RIAs and other fundamentalistas have been predicting that the bitcoin bubble will burst ever since it hit $1,000 but, as I’m writing this, BTC is worth more than $100,000. So much for fundamental analysis.

Even where fundamental analysis is applicable at first blush, the only way to definitively prove its validity is to backtest it on past data. Like, in the above example, Registered Investment Advisors should go back to the day on which the punter bought the stock based on finfluencer tips, gather the data for the company as on that day, carry out fundamental analysis, and show that it would have told him not to buy the said stock.

Even where fundamental analysis is applicable at first blush, the only way to definitively prove its validity is to backtest it on past data. Like, in the above example, Registered Investment Advisors should go back to the day on which the punter bought the stock based on finfluencer tips, gather the data for the company as on that day, carry out fundamental analysis, and show that it would have told him not to buy the said stock.

I don’t know a single RIA who offers to do backtesting. Without that, it’s hard to take fundamental analysis any more seriously than the advice to ignore tips from random finfluencers, especially in today’s world of AI.

While on that subject, it’s instructive to note that neither finfluencers nor RIAs give guaranteed returns. (PMS and hedge funds take a slice of the investor’s profits but they don’t share any of his losses, 100% of which are docked to the investor’s portfolio.)

Then there are many do’s and don’ts advised by practitioners of fundamental analysis. Let’s take the top three:

1. If it’s too good to be true, it probably is: History is replete with examples of investments that sounded too good to be true but eventually turned out to be true e.g. Dhirubhai Ambani Nylon Arbitrage, Sam Bankman-Fried Khimchi Premium, Sachin Bansal and Binny Bansal Flipkart Sale. Click here for more details.

2. Avoid investments you don’t understand: There are so many things we don’t understand in life but we do them because they’re means to ends that we seek e.g. As long as the light glows when we turn on a switch, we don’t need to know how electricity works. Likewise, investment is means to an end viz. wealth generation. While we can’t afford to be reckless, it’s naive to believe that a mere knowledge of financial products will drive wealth creation.

3. Choose simple products: There are no simple financial products. If you read contracts and get into details, you’ll discover gotchas even in elementary financial products like fixed deposit, locker, share, and mutual fund.

- The average depositor believes the money in his bank account belongs to him. It does not. Once deposited, the money belongs to the bank and what the depositor gets is an IOU from the bank to repay it on demand. If the bank goes bust, the IOU is only good up to the amount covered by deposit insurance (e.g. INR 500,000 in India, USD 250,000 in USA, GBP 80,000 in UK).

- On the other hand, the contents of a bank locker do belong to you as the customer. The locker contract specifies a long list of items that you cannot store in a locker (e.g. currency notes in India). If you do and are caught, you can’t escape prosecution by claiming that the bank accepted your stuff, so they must be kosher. Since the contents of a bank locker belong to you, the bank is not liable for what you keep in it.

But the locker itself belongs to the bank. There was a blade company down the street from my house. In addition to fixed deposits, it also offered safety vaults. When it went bankrupt, not only were the fixed deposits frozen (by the banking regulator) but so were the safety vaults (by the bankruptcy administrator), so customers lost access to both their funds and their belongings.

But the locker itself belongs to the bank. There was a blade company down the street from my house. In addition to fixed deposits, it also offered safety vaults. When it went bankrupt, not only were the fixed deposits frozen (by the banking regulator) but so were the safety vaults (by the bankruptcy administrator), so customers lost access to both their funds and their belongings.- Contrary to what the average shareholder thinks, their broker – not they – is the beneficial owner of their shares kept in custody in depostitory agencies like NSDL and CDSL. See Who Really Owns Your Shares? for more details.

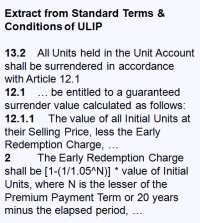

- In Puzzle Versus Mystery: Who’s To Blame For The Great Recession, I gave an example of a clause in the TOS of a mutual fund product that could not be understood even by the employees of the AMC that ran the fund!

tl;dr: There are no truly simple financial products. When you scratch the surface, almost all financial products are complex. I’ve always wondered why financial products never carry any warranty. I think I now know why.

As is evident, when the rubber hits the road, none of these guidances from RIAs can survive a tryst with the real world.

We spend hours doing research for buying clothes, gadgets, and other everyday items but we barely get to see a house for a few minutes before taking a decision to buy it. (Steal my idea: A genAI tool that scans a specific house location and reports on attributes that increase / decrease the attractiveness of the house for buyers and renters e.g. water supply, electricity outages, noise level, society rules, maintenance charges, etc.).

Likewise, we assess the value of everyday items at the point of purchase, buy them only if we’re convinced that their prices are worth it, and pay for them only after getting the goods. But, when it comes to a company’s share, we’re told that its price represents the discounted cash flows of the company in future, and are required to accept it at face value. We also need to pay the full money upfront to buy the shares and don’t have the comfort of waiting for the company to realize the cash flows in future and pay against those milestones!

People brazenly flout the standard operating procedures for making investments but many of them have still made fortunes on the back of these two asset classes, as I highlighted in Bombay Stock Exchange or Bombay Real Estate?.

In other words, most investments work out more often than not for most people.

Historically, financial regulators have blessed RIAs, not because of superior / assured outcomes, but due to their expertise and the transparent and regulated processes followed by them – unlike the often opaque methods of finfluencers. This preference made sense in the pre-AI era, when formal training and certification were the only credible proxies for expertise, and backstops for lack of assured outcomes. But today, in an age where ChatGPT aces competitive exams and performs sophisticated financial analysis, I’m not so sure if a RIA’s formal credentials are the only way to skin the investment cat.

The more I think about this, the more I’m reminded of what Hamlet told Horatio in the famous Shakespeare play!

It is important to exercise caution while making investments but gamechanging opportunities seldom wait for the average J6P to do fundamental analysis. As they say in venture capital, missing out on some deals can be a bigger mistake than overpaying for them.

“Missing out on a hot deal is a much bigger mistake in VC than overpaying for the same deal” ~ https://t.co/FE3YQlE14n.

Ergo FOMO / BAAP was the most profitable investing strategy during ZIRP. Time will tell how will it will work in the current HIRP era.— SKR (@s_ketharaman) September 24, 2023

This reminds me of my oft-expressed opinion that, while correlation is not causation, most opportunities suggested by correlation will be lost by the time causation is established. Per my conspiracy theory, people who keep saying “correlation is not causation” are either pedantic or opportunistic – quick to exploit the openings that correlation exposes, while urging others to waste time proving causation and thereby keeping the competition at bay.