Central Bank Digital Currency is digital cash.

Central Bank Digital Currency is digital cash.

Like paper currency notes, it’s issued by the central bank and does not bear interest. Also, like paper currency notes, it’s legal tender.

At its inception, CBDC was supposed to be based on the blockchain. We don’t hear much about that facet of it nowadays.

At least 130 countries have announced plans for CBDC.

Only commercial banks can have accounts in central banks. Individuals and businesses can open accounts only in commercial banks.

For the uninitiated, central banks are government organizations that, among other activities, print currency notes. Examples include Reserve Bank of India in India, Federal Reserve Board in USA and Bank of England in UK. Commercial banks include both public sector and private sector companies engaged in the business of collecting deposits and making loans. Examples include State Bank of India in India, JP Morgan Chase in USA, and Barclays in UK.

Balances in commercial bank accounts are insured up to ₹500,000 in India (by DICGC), $250,000 in USA (by FDIC) and £85,000 in UK (by FSCS).

Contrary to the popular narrative, banks are NOT custodians of our money – they’re our unsecured debtors. Once we deposit our money in a commercial bank, it can lend it out without informing us about – let alone take our permission for – the identity of the borrower, interest rate, tenor and other conditions of the loan.

If a commercial bank goes bust, depositors are entitled to get back only the insured amount (per person per bank regardless of number of accounts). In other words, they stand to forfeit all monies in excess of that. This is obviously a problem for many individuals and most companies who hold more deposits than the insured sum.

Enter Central Bank Digital Currency.

I first read about CBDC in MIT Technology Review a few years ago. In the article that I cannot locate now, the author introduced the concept of FedAccount, which is an account at Federal Reserve Board (which is the central bank of USA, as noted earlier). FedAccount can be opened by everyone, including individuals and businesses. The full CBDC balance in a FedAccount enjoys sovereign guarantee without any ceiling, which is another way of saying it’s totally safe.

At first, this was the only envisaged form of distribution of CBDC. It was later termed Retail CBDC for reasons that will become evident soon.

To recap, balances in commercial banks are not totally insured whereas the entire CBDC balance in FedAccount is.

This created a disconnect. Commercial banks feared that this “safety arbitrage” could entice their depositors to withdraw their money and move them to the central bank, thereby leaving them with no money to lend, which would bring the economy to a grinding halt.

There are also those who fear deposits might flee from commercial banks to the safe haven of CBDC at the first whiff of financial grapeshot. – Financial Times.

To address their concerns, central banks introduced a new model of distributing CBDC where retail and corporate accounts would continue to be held with commercial banks and only commercial banks would be permitted to have FedAccounts with the central bank. Instead of paper currency notes, the central bank would mint CBDC and distribute it via commercial banks. This distribution model was termed Wholesale CBDC. The original CBDC distribution model was named Retail CBDC to distinguish it from Wholesale CBDC. What was not said but likely was that even CBDC balances would be insured only up to FDIC limit since they’re held at commercial banks that don’t enjoy sovereign guarantee as against central banks that do.

Maybe because my first exposure to CBDC was in the context of unlimited sovereign guarantee, I felt disappointed with Wholesale CBDC, which lacked it. When I received invites from a couple of my banks to participate in CBDC Pilot, I thought “CBDC via Commercial Bank” was the height of oxymoron.

I know there are many implementations of CBDC but the only one that makes sense is where banks are disintermediated and people keep their account directly at central bank aka FedAccount. Ergo an invitation from my bank to join eRupee pilot seems the height of oxymoron. pic.twitter.com/eEi9DYHkh8

— Ketharaman Swaminathan (@s_ketharaman) May 11, 2023

Then the public discourse shifted to “paying with CBDC”. The way it would work, people would install a CBDC Wallet App on their phone and receive CBDC, which they could spend at stores instead of paying with cash. That sounded meh: If we can already pay with credit card, UPI and other cashless methods of payments, why use CBDC?

As highlighted by Finextra, CBDC struggled to gain adoption.

Over time, many industry insiders started wondering if CBDC was a solution seeking a problem.

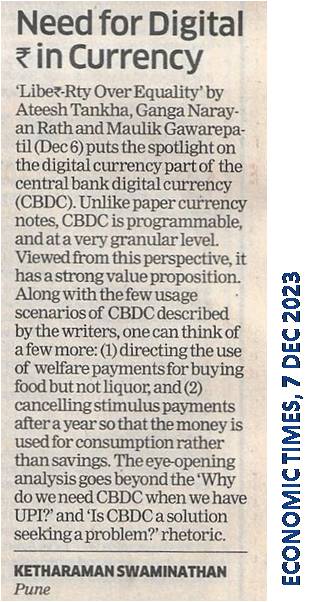

That changed after I read an op-ed entitled Libe-Rty Over Equality in a recent edition of The Economic Times.

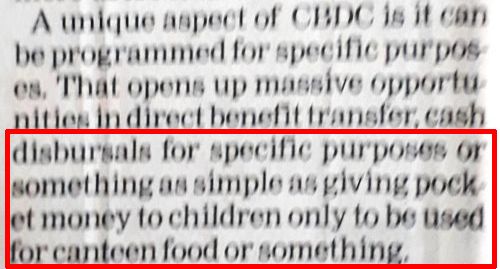

This is the first time somebody has put the spotlight on the Digital Currency part of Central Bank Digital Currency and highlighted that, unlike paper currency notes, CBDC is programmable. While CBDC and Smart Contract are distinct concepts, smart contracts can be used to program CBDC at a very granular level, according to ChatGPT. From that perspective, CBDC has a strong value proposition.

Experts have speculated many use cases for CBDC:

Government can program direct benefits such that the money can only be used to buy food – and not, say, liquor.

Government can program direct benefits such that the money can only be used to buy food – and not, say, liquor.- Government can cancel stimulus payments after a year so that people use the money for consumption rather than savings.

- Parents can issue allowance to their schoolgoing kids that can be spent only on tuck shop food – and not cigarettes.

I must hasten to add that restricting spends to categories has always been possible in cashless instruments like credit cards (pCard, MasterCard inControl) and Sodexo Coupons. Programmability now enables that to be accomplished in CBDC. Also, the above use cases may require new laws or changes to existing laws (not legal advice!)

As with any other technology, CBDC has its own pros and cons.

Pro Trackability of CBDC makes it easy to recover money stolen by cybercriminals in APP scam and other forms of cybercrime. Contrary to popular narrative, it’s not easy to catch cybercriminals even when they steal money via digital payments. While you can find the full details in my post entitled Why Is It Hard To Catch Cybercriminals?, suffice to say that legal jurisdictional issues pose challenges in identifying and freezing bank accounts before the scammer has moved the stolen money out. With CBDC, the notes are “marked” so to say, so banks can cancel them whereever they go. I must say that I like this approach to eliminate cybercrime even more than my Three Strike Rule.

Con In principle, government can track where people make UPI, FPS and Zelle payments. However, that requires subpoenas and court orders and can only be used selectively. CBDC is an open book in comparison: People’s spend data is readily available as records on a database controlled by the central bank. To that extent, CBDC takes surveillance to the next level. Not surprisingly, citizens in many countries are protesting against CBDC for gross violation of privacy. According to American Banker, Americans are pushing back against FedNow, the newly launched A2A RTP rail in USA, because they’re conflating it with CBDC and surveillance economy.

Con As mentioned earlier, paper currency notes don’t bear interest. Accordingly, physical cash is an interest-free loan to government and a direct tax on citizens. This tax is called seigniorage. In his op-ed in Financial Times titled The Real Scandal of Central Bank Digital Currency, noted British economist Andy Haldane observes that seigniorage is somewhat justified in paper notes since there’s a cost of printing and transporting physical cash. However, pointing out that those costs are absent in CBDC, he argues that there should be no seigniorage for CBDC. But, there is – since CBDC does not bear interest. Ergo, he calls it “the real scandal of CBDC”.

"The digits in your bank account stand for dollars, and you can pay with dollars by swiping your credit card. But those are debts that your BANK owes you. A true digital dollar would be a debt the US GOVT owes you, similar to a dollar bill." ~ @techreview.

Big difference!

— Ketharaman Swaminathan (@s_ketharaman) March 28, 2020

Pro / Con In theory, governments can freeze the accounts of terrorists. As USA did when Russia invaded Ukraine, a government can also weaponize its currency and cancel it via sanctions. In 2016, the Indian government went to the extent of demonetizing high value currency notes worth INR 15 Lakh Crore ~ $180B in order to flesh out INR 200 Crores ~ $25M held by terrorists and counterfeiters in cash. However, in practice, all of these actions require a huge administration machinery and / or cause tremendous hardships e.g. OFAC, subpoenas to commercial banks, compelling the common citizen to queue up in front of banks to withdraw their own cash, etc. Compared to CBDC, these are blunt instruments. Since CBDC can be programmed by the central bank, it enables governments to execute a precise surgical strike and cancel the CBDC bank balance held by unsavory – and only unsavory – characters without getting court orders, directing commercial banks, or troubling the Jane / Joe Six Pack. That’s obviously a pro for governments. However, it’s easy to see how this can degenerate into a con for the citizen if a government uses the same programmability feature to zero out CBDC bank balances of dissidents, opposition members, and any other kosher parties who just prove to be a thorn on the government’s side.

Only time will tell whether CBDC will lead to a utopia or dystopia.

A condensed version of the above post was published by Economic Times in its edition dated 7 December 2023.

In case the op-ed referenced above is not available online or is paywalled, cf. following exhibit.