Every time a shiny new fintech product or service enters the market, finsurgents immediately predict the death of traditional banks.

But traditional banks always go laughing all the way to the – ahem – bank.

We saw this when mobile wallets were the rage 8-10 years ago. Finsurgents predicted that they’d kill credit cards. Didn’t happen. In developed countries with high credit card and POS penetration, mobile wallet is just another form factor for plastic that works on top of the same underlying card rails. There’s no question of mobile wallet killing credit cards.

One wannabe disruptor predicted 10+ years ago that iPhone5 will kill plastic. Well, we're now on iPhone 11 & guess what are the recent finserv products from Apple? (1) "Plastic" credit card (2) App that lets iPhones accept plastic credit card.

— GTM360 (@GTM360) September 21, 2020

It happened next with Online P2P Lenders about 5-6 years ago. Finsurgents predicted that they would kill traditional loans sold by banks. Didn’t happen. Instead, online P2P lenders are the ones who seem to be dying now.

"LendingClub, which went public in 2014 at a market cap higher than all but 13 US banks has since lost ~90% of its value." ~ https://t.co/gPavmqC0zR via @business .

Moral of Story: You can't build a business out of giving a loan to someone just because they need it.

— GTM360 (@GTM360) December 27, 2019

“Buy Now Pay Later” is the latest shiny new toy.

In BNPL, consumers buy a big ticket item upfront and pay for it in one to three or more Equated Monthly Installments (EMIs) over the following months. To that extent, BNPL is just a new name for the good old installment purchase schemes offered by retailers and banks for ages. As Antony Jenkins, former CEO of Barclays, and a leading fintech entrepreneur, says “BNPL is point of sale financing that’s existed for 100 years”.

Nope. https://t.co/pxoHFDmLlr

— Bryan E. Clagett (@Clagett) December 15, 2020

Finsurgents are going gaga about BNPL. They’re predicting that Affirm, Klarna, PayPal and other leading BNPL companies will suck out the spend currently captured by credit cards and leave traditional banks high and dry.

Just not gonna happen.

In the USA, BNPL value in 2020 was $25 billion, which is a tiny fraction (0.7%) of the $3.6 trillion annually processed with credit card.

BNPL accounted for 0.7% of total credit card $ volume in 2020. BNPL-related purchases in the US for 2020 were roughly $25b, credit card volume $3.6 trillion.

And this doesn't account for ppl who paid their BNPL bill with a CC.

So, no–BNPL didn't play a role. https://t.co/9B7tn3wKR0

— Ron Shevlin (@rshevlin) March 14, 2021

And then there are people who pan banks for underestimating BNPL.

It’s a great example of how incumbents underestimate the difference small details can make. Having merchants subsidize the interest rate, plus integration at the point of sale is disruptive. No way I’m keeping a balance on my credit card for a $2,800 peloton.

— Charlie Kroll (@CharlieKroll) November 30, 2020

Contrary to what the above tweet says, both Credit Card and BNPL support integration at the point of sale (at least in India). A customer reaching checkout can opt for repayment via installments on their credit card. Just as they can opt for BNPL.

The real difference between banks and BNPL lies not at the point of sale but at the point of aisle.

BNPL companies employ sales reps who hover around the shopfloor of electronics, home improvement, and other stores that are in their primary target audience. Tipped off by a Retailer’s sales rep, BNPL reps approach the Customer at the aisle and close the deal before she reaches the point of sale and gets the chance to opt for EMI schemes offered by banks on Credit Card.

Since banks don’t employ sales reps at these stores, they can’t waylay the customer at the aisle. Ergo they lose the loan business to BNPL providers.

The way BNPLs are currently operating, they could be termed providers of “point of aisle” rather than “point of sale” financing!

But sales reps cost money. Fintechs can afford to eat the cost because their new-age valuation-driven, venture capital-funded business model (“VC”) allows them to make losses. But banks can’t – their traditional business model is predicated on revenues and profits (“PLBS”) does not allow them to make losses.

Therefore, I don’t believe banks have underestimated BNPL. It’s just that the retail banking business model does not permit them to compete head-on with pure-play BNPL providers. In addition, because it’s not covered by TILA (Truth In Lending Act) regulations, BNPL leverages Regulatory Gap that most traditional banks won’t (at least not in the pursuit of innovation). For the uninitated, a Regulatory Gap is something that’s neither permitted nor banned by law.

But that does not mean that banks are losing money because of BNPL. In fact, it’s quite the opposite. There are at least three reasons why BNPL is enriching banks:

- In one of those quirks of consumer behavior, many BNPL customers settle their BNPL installments with their – ahem – credit card – and pay the standard interest and fees to banks. In addition, since the BNPL provider becomes the Merchant of Record for these payments, banks also earn interchange revenue from these transactions. Click here, here, here, and comments here for anecdata about this trend and the associated point that many BNPLs do not insist on auto-debit of repayments or even on customers to provide a funding source at the time of approving them for loans. To take my own example, I recently got approved for Amazon’s BNPL product called Amazon Pay Later without submitting any credit card / debit card / bank account details.

While BNPLs source the bulk of their funds from venture capital, it’s widely believed that they also borrow money from banks. I got a first hand confirmation of this when I saw the logo of Karur Vysya Bank on the approval letter issued by Capital Float, the lending partner of Amazon Pay Later BNPL. So, banks generate interest and fee income from BNPL firms instead of from the end consumer. The BNPL has merely redistributed the revenue from the Retail Banking SBU of a bank to its Business Banking SBU

While BNPLs source the bulk of their funds from venture capital, it’s widely believed that they also borrow money from banks. I got a first hand confirmation of this when I saw the logo of Karur Vysya Bank on the approval letter issued by Capital Float, the lending partner of Amazon Pay Later BNPL. So, banks generate interest and fee income from BNPL firms instead of from the end consumer. The BNPL has merely redistributed the revenue from the Retail Banking SBU of a bank to its Business Banking SBU- Many banks invest in Fintechs, either directly or via VC funds that invest in Fintechs. Due to frothy valuations enjoyed by Fintechs, VC funds deliver 15-20% returns to their Limited Partners a/k/a Investment Banking divisions of banks. Therefore, whatever interest and fee incomes that are lost to BNPLs by the Retail Banking SBU of a bank are more than made up by the MOIC (Multiple On Invested Capital) earned by the Investment Banking SBU of the same bank.

Therefore, BNPL is redistributing money from one part of a bank to another.

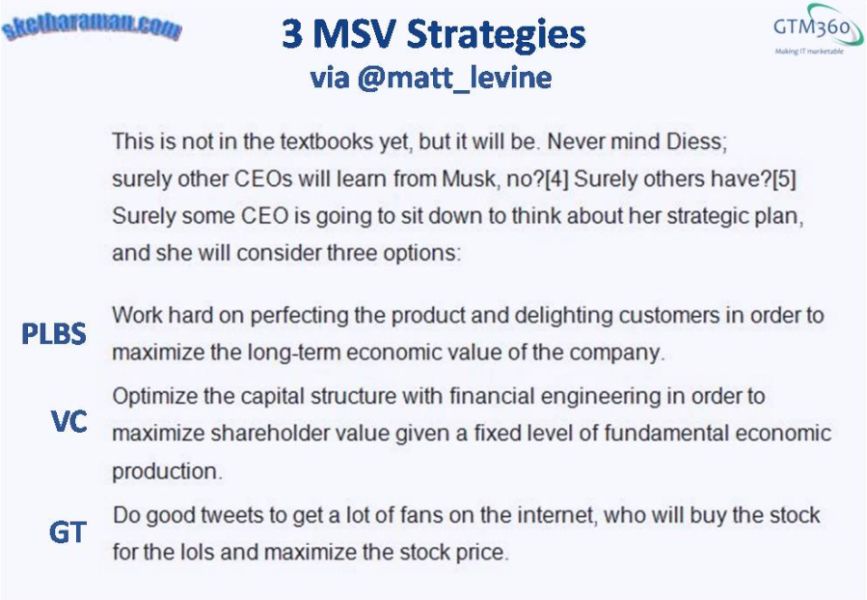

Just like SPAC. Many people predicted that this new fangled acquisition vehicle called Special Purpose Acquisition Company would disrupt the investment banking business of traditional banks by cutting them out of lucrative IPO fees. But, in reality, SPACs are not doing any such thing. As Matt Levine notes in a recent edition of his Money Stuff newsletter:

I have said this before, but I cannot get over how good the recent trend to cut banks out of initial public offerings has been, for the banks. It is one of the great accidental scams of modern finance. People got mad that investment banks get big fees for taking companies public, so they said “what if we found a new way to go public, one that reduced the power of the banks?” And the banks put on trench coats and fake mustaches and went to companies and whispered “you could do a direct listing, or go public by merging with a special purpose acquisition company; that’ll show those evil banks!” And then companies started doing that, and the banks laughed uncontrollably and raked in so, so, so much money.

In effect, SPACs are redistributing revenues from one part of a bank to another.

Ditto BNPLs.

Therefore, I’m convinced that BNPL won’t kill banks. If anything, it will enrich banks and become one more exhibit for the Jethro Tull song Banker Bets, Banker Wins.