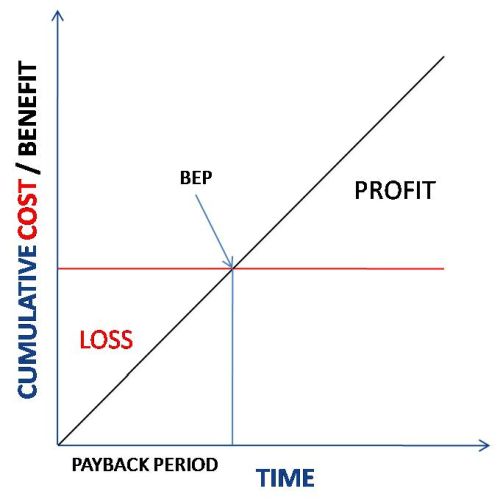

A company that invests in ERP stands to gain from higher inventory turns, lower DSO, etc. Benefits of enterprise software are generally of the nature of increase in income and / or reduction in expense.

To calculate the ROI of its investment, the company would add up the dollar value of the total benefits and divide it by the total cost of ownership of the ERP solution.

ROI = Benefits / Cost * 100%.

If we take the common case of an onprem ERP with frontended AMC, the cost is incurred onetime (see footnote 1).

Most companies roll out their ERP in phases, starting from a couple of functions in one SBU and expanding it in phases to all functions across all SBUs. As a result, the benefits of ERP accrue over a period of time. Therefore, the returns rise cumulatively from year to year.

At a certain point, the benefits will equal the cost, and the benefits-to-cost ratio will become 1 i.e. 100%. That point is called Break Even Point and the period is called Payback Period (see exhibit on the right). We say that the company has fully recouped its investments in ERP by then, and whatever benefits it gets subsequently go straight to its bottomline.

(It’s another question whether the company will publicly acknowledge the milestone. In the 50 years of existence of ERP, I can’t think of too many companies that have gone on record about their ROI from the technology. Against that backdrop, all this talk of ROI of AI is highly premature. In my 40 years of selling B2B technology, I can’t think of a single technology that has delivered ROI within three years of launch.)

Some people have extrapolated the above calculus of ROI for investments in a technology to ROI for investments in a technology company.

Some people have extrapolated the above calculus of ROI for investments in a technology to ROI for investments in a technology company.

Take journalist Karen Hao for example. In her recent book Empire of AI, she argues that the massive investments made by investors in AI labs cannot be recouped from consumer and enterprise markets and advances that as a reason for AI vendors to pursue government customers (since government has unlimited funds).

This logic is flawed.

When somebody invests in a company, they have three sources of returns:

- Dividends paid by the company out of its profits.

- Appreciation in the company’s stock price.

- Increase in their own market cap driven by the investment.

As you can see, these are unrelated to higher inventory turns, lower DSO, and other benefits accruing to customers who invest in the technology.

Back in the day – say until the mid 1990s or so – dividend was the primary source of returns for investments in shares of a company.

But, since the turn of the millennium, growth has overtaken profitability as the primary goal of companies in high-growth industries. Stock prices of tech companies have risen as long as they’ve grown, and their investors have gotten huge returns despite their giving no dividends e.g. AirBnB, Uber, and dozens of other tech companies that went public in the last 20 years or so. (I recently learned that even Google did not pay any dividend until recently).

Now take Microsoft. The company invested a total of $13 billion in OpenAI. While OpenAI still makes losses and does not give any dividend to Microsoft, its valuation has skyrocketed since its founding, and Microsoft’s share in the AI lab is now worth $147 billion, thus yielding a surplus of $134 billion ~ MOIC (Multiple In Invested Capital) of 11X. (Source)

Furthermore, due to its early investment in OpenAI, Microsoft is perceived by the markets to have a huge lead in AI. This has resulted in Microsoft’s market cap growing by around $2.5 trillion during the same period.

So, while Microsoft has not received any dividends from its investment in OpenAI ($13B), it has received massive benefits from the investment in the form of rise in the valuations of OpenAI and itself ($2.634T).

Another example is Twitter nka X. Elon Musk bought the firm for $44 billion. At one point, its shareholders had marked its valuation down to $9B. Then Musk opened an AI lab (xAI) and did a reverse merger with X and the combined entity is now worth $135B. Many investors who funded Musk’s $44B acquisition have the choice to cash out their share of Twitter stock at this 3X valuation – it’s another story that many of them have chosen to hodl.

“A well run tech company is 2X overstaffed; a badly run tech company is 4X overstaffed” is an old SV saying. BigTech CEOs started taking it seriously after Elon proved its validity by slashing the headcount of Twitter nka X from 8000 to 1800 and still shipping more features.

— SKR (@s_ketharaman) September 7, 2025

Technology does not have shares whereas technology company does.

As a result, technology is not tradeable but technology company is tradeable (see footnote 2).

Tradeability injects buoyancy. Ergo

ROI for Investment in Technology ≠ ROI for Investment in Technology Company

We’ve seen this with crypto and meme stocks. We’re seeing it in AI: Investors in AI companies have got massive returns. According to Economic Times:

Big Tech is spending more than ever on artificial intelligence – but the returns are rising too, and investors are buying in. AI played a bigger role in driving demand across internet search, digital advertising and cloud computing in the April-June quarter, powering revenue growth at technology giants (and AI investors) Microsoft, Meta, and Alphabet.

According to Bloomberg,

- Amazon earned $9.5 billion in pretax gain from its $8 billion investment in Anthropic.

- Alphabet reported $10.7 billion gains on equity securities, part of which came from its investment in Anthropic.

With returns exceeding investment, Amazon has crossed the BEP for its investment in Anthropic.

As a matter of fact, even some AI infrastructure vendors have got ROI. This is via drag revenue where a company is able to boost its revenue by infusing AI into its non-AI core offering. Microsoft Azure is a good example.

Microsoft’s Azure cloud revenue surges as AI spending pays off. Microsoft’s Azure cloud-computing business delivered another quarter of blockbuster growth on Wednesday, powering revenue above Wall Street’s expectations and showcasing the growing returns on its massive artificial intelligence bets. – Economic Times.

Depending on the source you trust, drag revenue for Microsoft was $15-30 billion for the last fiscal year.

Ditto investment bankers:

AI is proving a godsend to investment bankers – and not because it’s saving them time (although it may be doing that). A growing number of older enterprise software firms are snapping up AI minnows, in hopes of strengthening their own businesses. The latest was Workday’s $1.1 billion acquisition of Swedish firm Sana, which makes AI agents, services that take action on user’s behalf. The deal follows Atlassian’s purchase of an AI browser, The Browser Co., for $610 million and ServiceNow’s $2.85 billion acquisition of Moveworks, which sells AI assistants to deal with IT request tickets. Bankers are predicting more such deals. – The Briefing by @mvpeers via The Information.

Eventually, customers of AI would need to realize ROI for their investments in the technology for AI to cross the chasm and go mainstream, but that can follow a different timeline, and lack of ROI for customers does not imply lack of ROI for investors.

%age of Cos that rated their ERP project a success:

* 2015: 58%

* 2019: 88%.Key Reason for Sharp Increase: “To avoid reputational damage coming from failure, cos redefine success as whatever they get.” Now you know why aspirational selling works. https://t.co/fKX1hjD4t1

— GTM360 (@GTM360) April 16, 2020

On a side note, I’d once highlighted why it’s not easy to calculate the ROI for technology. That blog post referred to ROI for customers.

For investors in technology, it’s fairly easy to compute the ROI for their investments. Besides, if they’ve backed the right technology and the right company during the right zeitgeist, investors might even achieve their ROI quite fast.

Regarding the reference to government in the aforementioned book, government has always been a big buyer of technology since the dawn of Silicon Valley (see footnote 3). If not among the top three, government is certainly among the top five sectors of technology buyers. IT vendors have always sold their wares to government. AI companies are doing it now. Targeting government is not a sign of lack of consumer and enterprise markets, as the author of Empire of AI claims.

Regarding the reference to government in the aforementioned book, government has always been a big buyer of technology since the dawn of Silicon Valley (see footnote 3). If not among the top three, government is certainly among the top five sectors of technology buyers. IT vendors have always sold their wares to government. AI companies are doing it now. Targeting government is not a sign of lack of consumer and enterprise markets, as the author of Empire of AI claims.

Another important point to note is that many revolutionary technologies of the past were funded partly by government e.g. Internet by DARPA. Unlike them, all the capital invested in AI is from private sources like BigTech, PE and VC.

Karen Hao’s FUD on AI is a nothingburger.

Microsoft has not invested cash in OpenAI. Instead, it has issued Azure Credits to OpenAI. When OpenAI runs its models on Azure Cloud, it defrays these Azure Credits and Microsoft gets revenues. This is another source of returns for investment in a technology company that’s not available for investments in a technology. While this is not an entirely new investing playbook, the amounts involved in the case of genAI take it to a new level. More on this in a follow-on post. Watch this space!

FOOTNOTE(S):

- While SaaS ERP is very much in vogue, a vast majority of the installed base of ERP solutions is still COTS (Commercial Off The Shelf) and is subject to a onetime license fee. Even Gartner has used the same pricing model for ERP in this El Reg article: “ERP has straightforward up-front costs: You pay to license and implement it, then to train people so they can use it”.

- Shares of public companies have always been tradeable on stock exchanges (by definition). Nowadays, financial enginering innovations are enabling even private company shares to trade publicly e.g. Destiny Tech100 Inc, a publicly traded fund (NYSE: $DXYZ) comprising 100 high growth private firms like OpenAI, Revolut, and SpaceX.

- Despite being an Oracle alum, it was only recently that I learned that (a) CIA was the first customer of Oracle, which was founded 48 years ago in 1977, and that (b) the company got its name from an internal CIA project! (H/T @ByrneHobart).