There are many terms that don’t mean what they say.

- Some are misnomers e.g. Nonprofit

- Others sound broader than they are e.g Insider Trading

- Still others are obfuscatory e.g. KYC.

I’ve coined the term WYSINWYG to represent such terms.

As you might have guessed, WSINWYG (to be pronounced “wisinwig”) stands for “What You See Is Not What You Get” .

We’ll cover four WYSINWYGs from finance in this post.

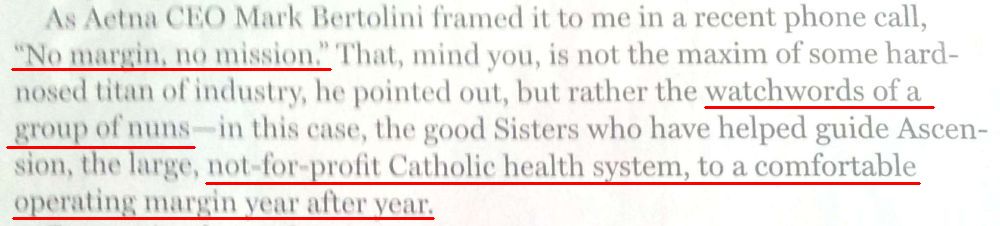

#1. NONPROFIT COMPANY

Nonprofit company does not mean that the company cannot or does not make profit. Many nonprofit companies do make profits. Some of them even make whopping profits e.g. Kaiser Permanente in USA and National Payments Corporation of India (NPCI) in India.

"Not-for-profit Kaiser Permanente made a whopping profit of $3 billion" ~ https://t.co/IxlWrq31TP .

Gentle reminder that a not-for-profit company can make profits, even whopping profits. To find out what is not for profit about it, see https://t.co/9OdfX3lyZ6

— Ketharaman Swaminathan (@s_ketharaman) July 8, 2020

Even nonprofit religious organizations make profits e.g. Ascension, the Catholic helath system.

Nonprofit means that the company cannot distribute its profits to its shareholders by way of dividends. In other words, shareholders cannot profit from their shareholding in the nonprofit company. Nonprofit is actually a tax status, not a business model.

#2. WINNER TAKES ALL

“Winner Takes All” does not mean monopoly / 100% market share.

The term is used to describe the “power law” market condition whereby very few companies in a certain sector (say, 20%) have most of the valuation / market cap (say, 80%) of that sector. It does not mean monopoly or duopoly where the entire market is owned by one or two companies respectively.

Driving Winner Takes All is the goal of VC. It has already been achieved in VC-backed industries like ecommerce (Amazon, Flipkart), Rideshare (Uber, Ola), Food Delivery (Swiggy, Zomato) and is on the way to being achieved in EdTech (Byju’s) and other startup categories.

Driving Winner Takes All is the goal of VC. It has already been achieved in VC-backed industries like ecommerce (Amazon, Flipkart), Rideshare (Uber, Ola), Food Delivery (Swiggy, Zomato) and is on the way to being achieved in EdTech (Byju’s) and other startup categories.

On a side note, a few years ago, many people said India / USA / UK are very big markets and will support multiple companies in any given industry. In other words, they argued against Winner Takes All happening. Well, they’re wrong because, as we saw above, it has already happened in a number of VC-backed industries. The point these people missed is, the survival of VC depends on Winner Takes All, so if VC cannot drive that outcome in a certain sector, it exits that sector and we wouldn’t be talking about it.

While the term has gained a lot of buzz due to VC, the fact is, Winner Takes All has been observed even in dowdy old industries like Insurance, just reckoned by a slightly different metric viz. Economic Profit, which is defined below.

Never thought "Winner Takes All" applied to the Insurance industry. But, according to @McKinsey , it does. Its analysis of the "economic profit of 209 insurers identified a power curve".

(Economic Profit = Profit – Charge for Capital used to get that Profit) pic.twitter.com/EF5809PI1X— Ketharaman Swaminathan (@s_ketharaman) July 19, 2019

#3. BANKING THE UNBANKED

“Banking the Unbanked” is not about giving people a compelling reason to open a bank account.

It refers to the situation when people don’t have a bank account because

- Banks refuse to open bank account for them

- Banks charge fees that they cannot afford.

In this context, “unbanked” has never been a problem in India. That’s because the government owns 70% of banks in India and, by regulatory diktat, mandates that banks

- Cannot refuse bank accounts

- Must offer at least one fee-free bank account.

These conditions are absent in the advanced nations. Since banks are entirely in the private sector in USA, UK, etc., they can jolly well decline bank accounts and refuse to offer fee-free bank accounts. As a result, a sizeable percentage of the population in the West was historically unbanked and became banked only recently by neobanks like Chime and Varo.

While PMJDY is a recent example of fee-free account, no-frill accounts of similar nature have been a common fixture in the Indian banking landscape for as long as I can remember (which is 45-50 years).

Going by that context, UPI did not bank the unbanked. In fact UPI will work only if the user already has a bank account, of which there were close to a billion when UPI was launched in 2007. While UPI elevated the use of digital payments to the next level and has reportedly brought down the use of cash in retail payments from 90% to 60%, it was never meant to bank the unbanked.

See the following thread on Twitter for more details.

@GergelyOrosz: If you truly want to “bank the unbanked”, look to what UPI did in India, Pix in Brazil, M-Pesa in Africa – all in a few short years.

@s_ketharaman: Tons of Kenyans didn’t have bank accounts. By giving them accounts and letting them make digital payments, TELCO-owned M-Pesa “banked the unbanked”. India already had one billion bank accounts when UPI was launched. While it took the usage of digital payments to the next level, it did not bank the unbanked.

@KetanD82: But with its ease of use, it certainly encouraged the unbanked or newly banked to use banking.

@s_ketharaman: UPI encouraged people to use digital payments, not banking. Even before UPI, hundreds of millions of Indians had a bank account, paid and got paid by cash, deposited cash in bank account, etc. All of that is banking.

@KetanD82: Digital payments made banking accessible to everyone. The road side tapari wala can use his bank account without visiting the bank. The entire eco system works without anyone visiting the bank. That’s what I mean by making banking accessible and democratized.

@s_ketharaman: That’s “unbranching the banked”, which is different from “banking the unbanked”, which has never been a problem in India as government owns 70% of banks and banks cannot deny a bank account to anyone.

@harMaal10: You are ignoring second order effects. A roadside fruit seller who won’t have required a bank account to function before is nudged towards considering opening one because customers are asking for convenience of paying via QR codes.

@s_ketharaman: They’re NOT SOEs. Unbanked

= banks refuse account or fees are too high for people to afford account.

≠ lack of compelling reason to have account.

Compared to most countries, India never had an unbanked problem.

On a side note, India is a highly underserved market for credit. Testimony: For a population of 1.4 billon people, there are only 80 million credit cards. (In 2019, there were only 40 million credit cards in India. In the first 50 years of credit cards, the industry issued 40M credit cards. In the next three years, it issued an equal number. While UPI has grown manifold since its inception, it’s at the cost of cash and cheques, not credit card, whose count has doubled during the same period.)

If someone coined such a term, this would be called “uncredited” – but it’s not “unbanked”.

I called out the undercredited nature of India four years ago in in my blog post entitled When Will Fintechs Sell What Customers Want To Buy?. Since then, dozens of fintechs have exploded on to the scene with BNPL products for both ecommerce and brick-and-mortar retail e.g. slice, UNI, ZestMoney. They have substantially increased the credit supply in the Indian market. This can be called “crediting the uncredited” – but not “banking the unbanked”.

#4. TOO BIG TO FAIL

This is more of a business term but I’m sneaking it in here since its essence is related to finance.

People point to Kodak, Nokia, and other large companies to claim that no company is too big to fail. Their contention is based on a literal interpretation of the TBTF phrase.

Nothing is too big to fail ever. If Nifty 50 companies like DHFL, kodak can fail what are startups.

— Dr. Ikjot Singh (@drikjotsingh) August 20, 2022

In truth, there are companies like AirBnB, Air India, BSNL, Uber, Wachovia, and YES Bank. Some of whom broke the law but were too influential to be shut down and the others were so strategic that their closure would have caused the risk of contagion. These companies were allowed to survive either by amending the laws to regularize their business models ex post-facto or with bailouts funded by taxpayer money.

Ergo “too big to fail” is very much a thing in practice. Just that it doesn’t mean what it says. IMO:

- “Too big” means influential and / or strategic, not necessarily big

- “To fail” means shut down, not perform poorly.

While on the topic, even Kodak and Nokia are still alive. While Kodak may be a pale reflection of its former self, Nokia is still a Fortune Global 1000 corporation with $26.72 billion in revenues and $32.45 billion in market cap.

We will cover four more WYSINWYG finance terms in a follow on post. Watch this space!

DISCLAIMER: This is not legal or financial advice.