Sorry for the headline bait but after last year’s headline When Will M&A Propel An Indian IT Company Into Fortune Global 500?, I couldn’t think of a better way to express the role of M&A in ushering the Indian IT industry into the doorsteps of the elite league of the world’s top 500 companies this year.

Before we do a deep dive into the industry, here are some basic facts and figures of the latest FORTUNE GLOBAL 500.

FORTUNE GLOBAL 500

The companies on the list together generated $41.7 trillion in revenue. This represents more than one-third of the world’s GDP.

The average Fortune Global 500 company generated a revenue of $83.4 billion.

Walmart is #1 on the list for the 12th consecutive year. The 500th company on the list this year is Heineken. Together, the two companies bring up the contours of Fortune Global 500 for 2025:

Fortune Global 500 earned $2.98 trillion in profit (in its second-most-profitable year ever).

Going by the loud proclamations made by finsurgents 10-15 years ago, traditional banks and financial institutions should be dead by now. But they’re not. Contrary to what Wannabe Disruptors predicted, financial services is not only alive but thriving and made $1 trillion profits. For as long as I can remember, financials has been the most profitable industry in Fortune Global 500.

The behemoths on the list have held their ground. According to Alyson Shontell, Editor-in-Chief of Fortune Magazine,

Studying the Global 500 from one year to the next rarely inspires radical new insights about the companies that power the world, because major shifts in the ranking are rare on that timescale. Even when you look back decades, you don’t see big surprises. That’s largely because of the staying power of the stalwarts of business – FORTUNE 500 DIGEST.

That said, the list has seen some big movements lower down the ranks. Meta, for example, jumped up 25 spots to # 41, while AI chipmaker Nvidia rose nearly 100 spots, to # 66. The changes could signal a big shakeup ahead as AI becomes more established.

TIL the backstory of Fortune Global 500, which was first published in 1990:

Fortune has published its flagship Fortune 500 list, ranking the largest U.S.-based companies by revenue, since 1955. For the first couple of decades, the research staff focused its efforts on American companies. Then, in 1976, the magazine began tabulating a separate international list of non-U.S. companies alongside the annual domestic list. As the turn of the century approached, globalization was progressing rapidly, and entirely separating the U.S. and non-U.S. lists started to make less sense. “Now that the global village is truly upon us, it looks more like a global industrial park,” wrote Fortune reporters Jung Ah Pak and Sally Solo in the July 30, 1990, issue. So the first edition of the Fortune Global 500 debuted in 1990, combining U.S. and non-U.S. companies in one ranking.

INDIA IN FORTUNE GLOBAL 500

As in the previous years, Reliance Industries (#88) is at the top of the list of Indian companies on Fortune Global 500.

ICICI Bank enters the list this year at #464.

The total number of Fortune Global 500 companies out of India remains unchanged at nine. That’s because Rajesh Exports exited the list.

Totally tracks the number of FORTUNE GLOBAL 500 companies:

– USA: ~140.

– China: ~ 130.

– India: 9.

I’ve been tracking this list for 30 years. Interestingly, while India’s GDP has skyrocketed by probably 10X since then, the # of Indian FG500 corporations has never crossed 10.— SKR (@s_ketharaman) August 10, 2025

On a side note, ICICI Bank recently announced an increase in Minimum Account Balance in savings accounts from INR 10,000 to INR 50,000 in what’s reported as a bid to shun the masses and lure the rich. Not sure if that’s a leading indicator or trailing indicator of the bank becoming one of the 500 largest companies in the world:).

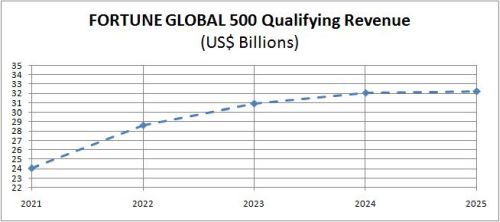

FORTUNE GLOBAL 500 QUALIFYING REVENUE

The Fortune Global 500 Qualifying Revenue rose by 0.53% to $32.249B.

For the uninitiated, Fortune Global 500 Qualifying Revenue is the revenue hurdle that a company must cross to enter the hallowed corridors of the 500 largest corporations in the world. In other words, it’s the revenue of the last company on the list i.e 500th rank holder.

FG500-QR has grown YoY every year in the last decade except in 2016 and 2021. The latest year’s growth rate (0.53%) is the lowest positive growth rate I can recall in the last 10 years. It’s another trigger for this post’s clickbait headline!

INDIAN IT INDUSTRY

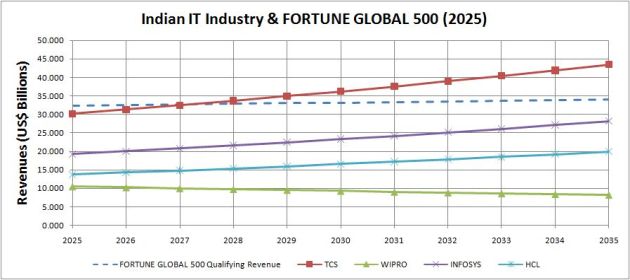

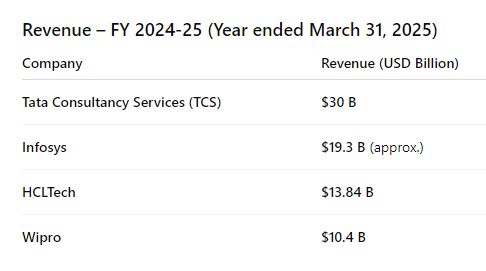

The league table of the Indian IT industry remain unchanged: TCS, Infosys, HCL, and Wipro continue to be the top four companies in the industry for FYE 2025 (i.e. 1 April 2024 – 31 March 2025). Their revenues for the last two financial years is given in the following exhibit.

As in the past, I forecasted the revenues of the four companies for the next 10 years by extrapolating their current CAGRs and juxtaposed them with the projected FG500 Qualifying Revenue for the same period. The following chart is the result:

(Click here to download the Excel model)

With a revenue of $30.18B, TCS is 6.42% behind FG500-QR of $32.249B. The gap between the two has narrowed for the third consecutive year (9.28% in FYE 2024 and 9.68% in FYE 2023). At present CAGRs, TCS will become a Fortune Global 500 corporation in three years i.e. FYE 2028. TCS will enter the list even earlier if it emulates its peers in doing big-ticket M&As (more on that in a bit).

(In the above chart, the TCS line seems to intersect the FG500-QR line a year earlier. That’s because the two figures for FYE 2027 are within a hair’s breadth of each other, just that TCS is slightly behind – FG500-QR @ $32.59B and TCS @ $32.46B.)

As in the past, I used regulatory filings and media reports to compile the revenues of the four companies in my model. Like always, it took a few hours, what with some companies reporing only INR figures that I had to convert to USD based on a suitable date for the exchange rate. But, emboldened by successfully using ChatGPT for tons of data analysis work during the past year, I asked it in parallel to compile these revenue figures. It came up with nearly-100% accurate results in seconds.

Apart from TCS (3.71%), Infosys (3.85%) and HCL (3.76%) have also surpassed the growth rate of Fortune Global 500 Qualifying Revenue (0.53%). Wipro (-2.51%) has not.

Infosys and HCL have acknowledged the role of M&A in their respective growth during FYE 2025: 80 bps in the case of Infosys and 50 bps in the case of HCL.

The key acquisitions of Infosys were InSemi, in-tech, MRE Consulting, and The Missing Link. Even as I write this, Infy announced a midsize acquisition: Versent of Australia.

The key acquisitions of HCL included HPE-CTG (Communications Technology Group of Hewlett Packard Enterprise).

(While HCL also acquired the assets of IBM Rational, that was before the current year.)

Without assigning any specific number, Wipro said that its $1.45B acquisition of Capco has helped accelerate the growth of its consulting business. Wipro and its founder also have a venture arm and an investment firm. Wipro Ventures and Premji Invest make strategic investments in enterprise software, AI, and other emerging and disruptive technologies. Some of their portcos include cutting-edge AI startups like Hippocrates, Poolside, and Galileo. Even as I write this, Wipro announced a big ticket M&A deal: Harman DTS of USA.

Last year, HCL (5.72%) had grown at a much higher pace than Infosys (1.93%) and was poised to overtake the current #2 on the league table during the ten year period of my forecasting model. That’s no longer the case: This year, HCL (3.76%) grew slower than Infosys (3.85%) and will not surpass the #2.

That said, both Infosys and HCL have a higher growth rate than TCS (3.71%), so they might overtake the current #1! I leave it to readers to do the math on when that would happen. (Hint: It’s well past the 10 year tenure of this model!).

The Indian IT Services industry continues to create IP in the form of frameworks, methodologies, and solution accelerators e.g. increase offshoring of ERP and enterprise software implementation from 0% to 80%.

Indian IT industry stopped relying on Labor Cost Arbitrage long ago. Most Indian IT Services companies have been using IP as a differentiator for over 10 years e.g. ASM 2.0, FENIX 2.0, DRYiCE, iONA SmartOps Platform, AppScan. https://t.co/rowYcxvnKv. HCL.

— SKR (@s_ketharaman) April 28, 2025

I never cease to be amazed by how randos on social media throw shade on the industry for not investing in R&D after publicly betraying their poor knowledge and low IQ, and making it obvious why the industry has followed the path that it has. Here are three exhibits of this behavior:

EXHIBIT 1:

Not fact-free. It’s well documented that Premji Invest has invested in tons of foreign AI companies like Hippocrates, Poolside, Galileo, etc.

If this is how Indian R&D carries out literature survey, no wonder Indian companies don’t invest in R&D in India. pic.twitter.com/8W3cP5py2V— SKR (@s_ketharaman) January 23, 2025

EXHIBIT 2:

ISRO and DRDO are public sector undertakings without much profit motive.

OP ran a pvt sector R&D firm with profit motive.

When gyaan givers don’t know the fundamental difference between the two, you don’t have to look far to know why Indian companies avoid R&D via Indian talent.— SKR (@s_ketharaman) August 10, 2025

EXHIBIT 3:

IT IS idiotic because it

(1) fails to understand that Indian IT Sector is in IT Services and not IT Product; the two have different DNA; no company is equally successful in both.

(2) stupidly rants against one successful sector when it should be seeking the start of another.— SKR (@s_ketharaman) August 10, 2025