Facing mounting GST notices, many small merchants in Bangalore and elsewhere in the state of Karnataka are declining UPI and other digital payments, and insisting on cash from their customers. They include streetfood vendors, pushcart sellers, and khirana stores (India’s version of mom-and-pop stores selling grocery).

Facing mounting GST notices, many small merchants in Bangalore and elsewhere in the state of Karnataka are declining UPI and other digital payments, and insisting on cash from their customers. They include streetfood vendors, pushcart sellers, and khirana stores (India’s version of mom-and-pop stores selling grocery).

This is causing major inconvenience to consumers who have practically stopped carrying cash ever since UPI went mainstream for retail payments 7-8 years ago.

For the uninitiated, GST or Goods & Services Tax, an indirect tax, is the VAT of India. Businesses selling goods must register for GST if their annual revenue exceeds INR 40 lakhs ($47,000) whereas the threshold for service providers is INR 20 lakhs ($23,500). According to ET NOW, the commercial taxes department has clarified that it issued GST notices only to those vendors who collected more than the above amounts via UPI.

In this blog post, I’ll cover a few topics related to this fracas.

1. Do small merchants make so much money?

There are reportedly 80 million unregistered businesses in India. Certainly a vast majority of them will not make so much money but, per personal experience and anecdata, a thin minority will.

There are reportedly 80 million unregistered businesses in India. Certainly a vast majority of them will not make so much money but, per personal experience and anecdata, a thin minority will.

There was a juice seller outside my office in the “Lands End” area of Bandra West in the then Bombay. Late evenings, cars used to be lined up literally all the way up to the end of land before Arabian Sea started. He used to have a couple of workers to deliver glasses of juice to the cars wherever they were parked. I don’t know if anyone kept a track of his sales volumes, cost, margin, etc., but it was rumored that he owned a couple of apartments in the tony Pali Hill area. This was in circa 1990.

Cue to the present day.

There’s a traveling streetside vendor who sells Idli and Vada in a couple of neighborhoods in Pune. I’m guessing his daily revenue is easily INR 10,000 per day.

Then there’s this Samosa-Vada Pav streetside vendor in Shivaji Market, the main market of Pune. Like many of his ilk, he wraps his products in a newspaper. After eating them, many customers chuck the newspaper here and there. The few conscientous ones look for a trash can. I read somewhere that tax officials surveilled the bin and counted the number of sheets of disposed-off newspapers inside it. From that, they arrived at an estimate of sales, costs and profits. Apparently, the figures suggested that the seller made way more money than the minimum taxable income.

"Millionaire hawker has 10 houses in Mumbai and two plots in UP." ~ https://t.co/u6hVug1qnO .

At last people will believe me when I tell them the streetside fruit juice seller outside my old Bandra office was rumored to own two apartments in Pali Hill.— SKR (@s_ketharaman) September 10, 2021

tl;dr: There surely is a thin minority of small merchants who earn more than the GST threshold for revenues. I’m guessing GST notices have gone out only to a tiny fraction of this thin minority.

2. Why refuse UPI?

Earlier this year, the media carried reports that GST department was planning to source income data from payment gateway companies who process UPI and other digital payments for small merchants. Apparently, the department identified one pani puri vendor who made INR 40 Lakhs via digital payments alone (in addition to an unknown amount via cash).

Pani puri vendor has an income of 40 lakhs via payment gateways. Imagine the money he must be making tax free https://t.co/MxKGncJgZH

— ?????? * (@ggganeshh) January 1, 2025

Merchants have sensed a strong correlation between their acceptance of digital payments and authorities’ knowledge of their incomes. That being the case, it’s obvious that small merchants who wish to stay out of the GST radar would want to refuse UPI and other digital payments.

The GST Department has made it clear that GST registration is mandatory above the aforementioned thresholds regardless of whether merchants collect payments in cash or via digital payments. However, it’s not easy to compute revenues if collections happen in cash. (But not impossible either, as saw in the Shivaji Market example above.)

3. Why avoid GST?

GST is a Levy-Collect-Remit (LCR) tax whereby merchant levies GST on top of his base price, collects the total amount from the customer, retains his base price and remits the GST to the government. Accordingly, merchant does not pay GST from his own pocket.

Given that the merchant passes on the cost of GST to consumers, why would he want to avoid GST?

According to news reports, merchants want to avoid the compliance headaches that come with GST registration and statutory filings. From personal experience with my company, I can confirm the part about headaches. From three statutory filings per year during the previous Service Tax regime, we now need to file three statutory filings per month under the GST regime plus three more annual reports once a year i.e. a total of 39 reports a year.

But I think this goes beyond administrative headaches.

4. Are small merchants evading GST?

Some rando on X fka Twitter claimed that small merchants are collecting GST from consumers but not remitting it to the government. I found this intriguing and decided to do a deep dive into it.

Packaged goods are subject to Maximum Retail Price regime in India. Sticker prices for B2C products include GST (whereas those for B2B exclude GST) (see footnote 1). Accordingly, MRP printed on FMCG goods in India includes GST.

The distribution channel for packaged goods spans multiple stages (see footnote 2):

Manufactuer —> Wholesaler —> Retailer —> Consumer.

I know for a fact that GST is added in the primary sale from Manufacturer to Wholesaler and the secondary sale from Wholesaler to Retailer. But I was not sure about the tertiary sale from Retailer to Consumer and about how MRP reflects multistage GST.

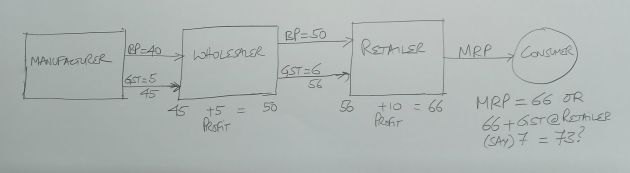

I decided to consult ChatGPT. I uploaded the following sketch and asked ChatGPT

- Whether GST is applicable for the retailer’s sale, and

- Would MRP be INR 73 (if applicable) or INR 66 (if not applicable).

ChatGPT replied that:

- GST is indeed applicable in the tertiary sale from Retailer to Consumer

- MRP would be INR 73.

(NOTE: ChatGPT could carry out data analysis based on handwritten content / unstructured data – this was a first for me.)

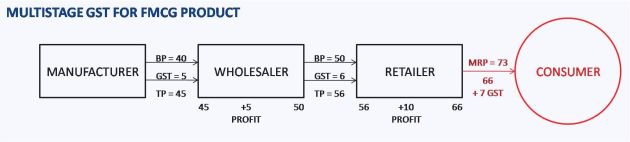

I’ve updated the above exhibit accordingly:

This rhymes with my experience of purchasing FMCG goods from big box retailers. Their bill shows the total selling price and provides the breakup of base price and GST. In this example, the bill would show:

Total Price: INR 73.

of which:

Base Price: INR 66.

GST: INR 7.

Now, a big box retailer is GST registered. It would collect INR 73 from the consumer, retain INR 66 and remit INR 7 less Input Tax Credit of INR 6 i.e. INR 1 to the GST Department.

What would a small merchant do?

Since he’s not GST-registered, he would not remit the INR 7 to GST Department. While he cannot claim Input Tax Credit, there’s still a GST leakage of INR 1.

It’s one thing for small merchants to not levy or collect GST because they refuse UPI and don’t come under GST regime.

But it’s another thing for them to collect GST that’s included in MRP and not remit it to GST Department. Not legal or taxation advice but this sounds like a more egregious form of GST evasion than is commonly perceived.

5. What about Income Tax?

If small merchants file as individual, income tax is applicable on revenue i.e. income. Netting off expenses is not permitted. But income tax is applicable only above the tax exemption limit of INR 12LPA ($14100).

+1. Money Quote: “These are not small limits for our country.”

Not sure how many people realize that the tax exemption limit (₹12L/$14K) of India ($2.6K PCI) is in the same ballpark as that of USA ($80K PCI), UK ($53K PCI) & Germany ($55K PCI).

Tax Enforcement ≠ Tax Terrorism.— SKR (@s_ketharaman) July 20, 2025

On the other hand, if small merchants file as business, they can net off expenses. Income / corporate tax is applicable only on profit. However there’s no tax exemption limit i.e. they’re liable to pay corporate tax from the first rupee of profit.

The tax demand notices that have gone out so far are for GST, not Income Tax. Per Chartered Accountant (CPA of India) grapevine, government looks the other way if net income is below INR 10 lakhs ($11765).

In this post, I’ve only covered the primary topics related to the Small Merchants UPI Ban controversy. There are many other secondary topics like simplifying GST registration, payment mode obligation on merchants, playbook for widening tax net, and so on. I hope to cover them in a follow-on post in the coming days. Watch this space.

DISCLAIMER: Nothing in this blog post is legal or tax advice.

FOOTNOTES:

- This is similar to the treatment of VAT in European Union (EU) and United Kingdom (UK) and contrary to the treatment of sales tax in USA where sales tax is charged extra on top of sticker price even for B2C.

- There could be more stages like C&F Agent and Distributor but I’ve skipped them since they don’t make a substantive difference in the context of this blog post.

UPDATE DATED 10 NOVEMBER 2025

I got another example of streetside vendor’s takings via X fka Twitter handle @naveenkopparam today.

@naveenkopparam: A street food dosa vendor in Mysore makes INR 20K on an average daily, totalling up to INR 6 lakhs a month. Excluding all the expenses, he must be netting at least INR 3 lakhs a month. Doubt if he pays a single paisa in income tax.