A banker quit his job and started a new company. He applied for a debit card for his company. Ram, as we’ll call the ex-banker, completed the required forms, submitted his company’s board resolution for the debit card and handed over copies of his company’s incorporation certificate, articles of association, and all the other documents required for KYC.

Why is it far more painful to get a mobile phone connection, debit card or Internet Banking in the name of a company than an individual?

— GTM360 (@GTM360) September 26, 2017

Nothing happened for two weeks. Then a Relationship Manager from the bank called Ram and asked him to resubmit the application. When Ram inquired why, the RM sheepishly admitted that his bank had misplaced all his documents!

When Ram mentioned this incident to me, I told him banks are not alone.

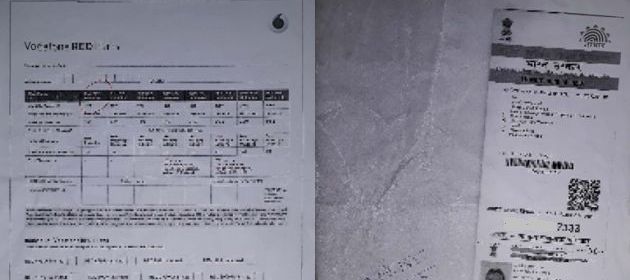

I narrated my experience with a leading Mobile Network Operator / TELCO. On a recent visit to its store to transfer my mobile phone connections to my company’s name, the store manager handed over a flyer with various corporate plans. While studying the plans at my office later, I happened to flip over the paper. I was shocked to find that it was someone’s Aadhaar Card copy.

It was presumably submitted by some other customer to fulfill his KYC. I know it’s “his” because I could read the name.

When I mentioned this experience to Ram, he recounted an old incident when he was still working at a bank. As a customer was walking past his branch, she noticed that her PAN card copy was being used to clean the glass windows of the branch! She stormed into the branch and gave him a piece of her mind. So, when his RM told him he had misplaced his KYC documents, this ex-banker took it on the chin as a taste of his own medicine!

I hope these are just isolated incidents of what happens to the KYC documents we submit to banks and TELCOs. I’d like to believe that, in general, our service providers take good care of our KYC documents.

For the uninitiated, customers need to submit KYC documents repeatedly in India – once while opening the account, each time they change a plan or buy a Value Added Service and periodically for RE-KYC. (I’d be remiss if I forget to call out Reliance Jio as the sole exception to this rigamarole to the best of my knowledge. As I’d highlighted here, India’s latest TELCO has only ever done KYC once and, that too, via an e-KYC process that was formless and didn’t call for any paper documents.)

eKYC eats both! I just signed up for Jio Prime. Still no form, no documents, no wet ink signature.

https://t.co/kh7IGdYqBX— Ketharaman Swaminathan (@s_ketharaman) March 11, 2017

As an aside, when it comes to documents submitted as collateral for home loans, I’m not so sure. A few years ago, many borrowers of a bank complained that, when they paid up their home loans and asked for the original property deeds back, their bank drew a blank. Apparently, the original documents stored by the bank at an offshore location were damaged during the rains.

In the wake of the recent fraud at leading public sector bank Punjab National Bank, there’s a major clamor to privatize banks. I’ve mixed views on this topic but I’m certainly not under the impression that everything is hunky dory at private sector banks.

All the three banks mentioned above are leading private sector banks of India.

UPDATE DATED 5 NOVEMBER 2018:

Looks like I was over-optimistic when I wrote “I hope these are just isolated incidents of what happens to the KYC documents we submit to banks and TELCOs. I’d like to believe that, in general, our service providers take good care of our KYC documents.”

According to today’s Pune Mirror, a retired cop’s Aadhaar Card has been misused by a leading MNO.