Contrary to popular belief, Flipkart didn’t pioneer ecommerce in India. That distinction belongs to Fabmall, the startup that introduced ecommerce in the mid-1990s well before Flipkart was founded in 2007. I remember placing orders from a dial-up modem in 1998 and paying online by credit card, which was the only mode of payment supported by ecommerce forerunners like Fabmall, Rediff and IndiaTimes Shopping.

That said, Flipkart did pioneer COD in India. The new payment method, launched in 2010, gave a huge fillip to ecommerce in India.

For the uninitiated, under COD, a customer orders online but does not pay online – instead they pay the delivery agent that delivers the goods. In the early days of COD, the payment at the customer’s doorstep happened by cash, ergo the term Cash on Delivery. However, with the proliferation of mobile POS and mobile wallets, many COD orders are paid for with credit card, debit card or mobile wallet nowadays. So COD could equally well stand for “Card on Delivery” or “Wallet on Delivery”. Given the variety of payment instruments actually used in a COD transaction, Cash on Delivery is a misnomer. Perhaps “Pay on Delivery” is a more accurate term for this method of payment now but that’s a post for another day.

Another characteristic of this method of payment – the customer pays only against receipt of goods and not at the time of order placement – is more relevant in the context of this blog post.

Initially, Flipkart and other ecommerce companies ascribed the runaway success of COD to low card penetration in India. Even the mainstream media went along with their claim that there were very few cards in India. Even at the time, this claim was highly patronizing – I used to pay for my online purchases a decade earlier by credit card. Today, it’s total BS: There are 40 million online shoppers and 870 million payment cards in India. So, there are enough and more cards for every consumer who wants to shop online in India.

Why does @vivwalt forget that there are >500M debit cards that can also be used to shop on Amazon India? https://t.co/6pi5BjT5Fq

— GTM360 (@GTM360) January 26, 2016

If low card penetration is not the reason for the overwhelming popularity of COD, what is?

Going by personal experience and anecdotal evidence, it could be friction and failed payments caused by two factor authentication. For the uninitiated, 2FA became mandatory for all online payments in India in 2009. For reasons explained in the below exhibit, 2FA stunted online payments and drove many long time credit card users like me to COD for online purchases.

Why Two Factor Authentication Is A “Conversion Killer” & “Blood Pressure Booster”

Any digital payment goes through a long value chain comprising multiple entities. Taking credit card as an example, the entities include Consumer (e.g. You), Merchant (e.g. Amazon), Acquirer (the bank that supplies the POS terminal and enables the merchant to accept card payments e.g. ICICI), Card Network (e.g. Visa / MasterCard), Issuer (the bank that issues the card and enables the Consumer to make card payments e.g. Citi), Electronic Payment Gateway (e.g. Bill Junction), Payment Service Provider (e.g. PayZapp) and Mobile Network Operator (e.g. Vodafone).

Each player processes a part of the payment and forwards it along to the next player in the value chain. To that extent, the card payment rails resembles a power train made up of several moving parts.

In a 2FA card payment, there are typically five moving parts. When a Consumer pays by card on the Merchant’s website, they’re shunted around from one moving part to another. One tells them to enter their card details (card #, etc.), another prompts them to enter their password (e.g. VerifiedByVisa), and another sends an OTP (One Time Password) to their mobile phone, and so on. The Consumer is confronted by several systems, each with a different UI, flitting around the screen, one after the other in rapid succession. This causes a lot of anxiety. In response, some Consumers abandon the payment midway. The Merchant loses business. Ergo Conversion Killer #1.

The remaining intrepid Consumers who brave the friction and complete the journey now rely on the various moving parts to go to work to process the payment. When all moving parts hum along nicely and complete their respective tasks, the payment succeeds. But even if one moving part is down, the payment fails.

In an ideal world, all servers will have 100% availability, all pipes will enjoy non-stop connectivity, and all software will be bug-free – enabling all moving parts to work 24/7/365 and process 100% of payments successfully.

But things are not so hunky dory in the real world. Cost and other constraints cap the uptime of each moving part to around 90%. That means an end-to-end 2FA transaction traversing five moving parts will will succeed only 59% of the time (being 0.9*0.9*0.9*0.9*0.9*100%). Ergo, a credit card payment subject to 2FA has a success rate of only ~60%. Which means, the Merchant loses 40% business. Ergo Conversion Killer #2.

The remaining 40% of 2FA payments fail, which means the Consumer’s account will be debited but the Merchant will refuse to ship / handover the ordered goods on the grounds that he hasn’t received the money. Ergo Blood Pressure Booster #1.

Failed payments fall into a “CyberAbyss” of sorts, which comprises Collection Account of Merchant, Nostro Account of Sender Bank at Scheme Operator, Nostro Account of Beneficiary Bank at Scheme Operator, Internal Collection Accounts at Sender Bank and Beneficiary Bank, Scheme Operator Account, Unintended Beneficiary’s Account, and dozens of other nooks and crannies in the payment value chain.

Some Merchants / Issuers use sophisticated tools and are mindful about Customer Experience. They will be able to ferret out failed payments from the CyberAbyss and reprocess them. Others don’t and won’t, so failed payments will remain stuck in the CyberAbyss.

Consumers of the first cohort will get their money back in their accounts automatically within a few days. Consumers of the second cohort will be made to run from pillar to post between the Issuer and the Merchant for several months to get a refund. Ergo Blood Pressure Booster #2. Consumers in both cohorts will think twice before hazarding another card payment in future.

In a nutshell, two factor authentication for credit card payments in particular and all forms of digital payments (e.g. Debit Card, FPS, NEFT, UPI) in general introduces tremendous friction and causes a lot of failed payments, thereby resulting in loss of revenues for Merchants and stress for Consumers. Ergo it’s called a “Conversion Killer” and “Blood Pressure Booster”.

Cue to the present day.

The Government of India demonetized high value currency notes in November 2016. On the back of the “Note Ban”, the government began pushing cashless payments. Trending as #CashlessIndia, the drive has resulted in the proliferation of several new digital payments such as UPI, BHIM, BharatQR and, most recently, Aadhaar Pay.

Bugs and all, @NPCI_BHIM app is a miracle in s/w dev. Similar apps in developed nations have taken months to develop & cost millions.

— GTM360 (@GTM360) January 6, 2017

Credit card, debit card, e-wallet, m-wallet, realtime A2A, biometric – you name it, India has it. I wouldn’t be bragging if I claimed that India has more types (and brands) of digital payments than any other country in the world today. Some of them (credit and debit cards, mobile wallets) involve incumbent banks and card networks (Visa, MasterCard and the indigenous RuPay) whereas others (UPI, BHIM and Aadhaar Pay) disintermediate card networks from the payment value chain. But I digress.

The important point here is some of the recently-launched digital payments have found innovative ways to enhance the CX of online payments and improve their success rates while still remaining compliant with the regulator’s two-factor authentication mandate. Think HDFC Bank’s PayZapp and PayTM.

The proliferation of frictionless digital payments has had an immediate and perceptible impact on brick-and-mortar retail. In a recent newspaper article, one of the doyens of the Indian organized retail industry attributed strong growth of his company’s topline to digital payments.

As a payments professional, I'm delighted to see a direct link between digital payment adoption & a company's topline. #CashlessIndia pic.twitter.com/xm9tAv3y9a

— Ketharaman Swaminathan (@s_ketharaman) January 19, 2017

But not on ecommerce, which still remains stubbornly driven by cash. According to latest reports, nearly 70% of online purchases are paid by COD, with some reports putting the figure as high as 83%.

70% COD in ecommerce is even higher than widely believed – or has the %age gone up in recent times? pic.twitter.com/kDqBr3Ev72

— GTM360 (@GTM360) June 6, 2016

If that sounds puzzling, it is – but only if you think of payments in an isolated context.

If you look at the end-to-end customer journey, payment plays another role: It acts as a seal of trust placed by the buyer on the seller. In plain English, you pay someone in advance only if you trust them to deliver later. It’s this facet of payment, which is unrelated to the mechanics of its operating model, that drives the dominance of COD.

From personal experience and anecdotal evidence in the recent past, cash still rules ecommerce in India because of the following trust-related factors:

#1. Delivery Address Ambiguity

While ordering a pizza on Pizza Hut’s mobile app, I reached the checkout page. I was asked to enter my building’s name. As soon as I finished typing in the first three characters of my building’ name (SAT), the app went into a tizzy. It recovered after 2-3 minutes and displayed a long list of buildings from which I had to select one. None of them matched mine. Ditto when I entered the first 3 characters of my street name on the next field of the checkout screen. Since I had to do something to move forward, I selected the option that came closest to my location. (No, the app didn’t allow freeform text entry of my building or street name). The app again went into a tizzy. When it came back, it displayed the delivery address the way it had reckoned it. This didn’t match my real address.

While ordering a pizza on Pizza Hut’s mobile app, I reached the checkout page. I was asked to enter my building’s name. As soon as I finished typing in the first three characters of my building’ name (SAT), the app went into a tizzy. It recovered after 2-3 minutes and displayed a long list of buildings from which I had to select one. None of them matched mine. Ditto when I entered the first 3 characters of my street name on the next field of the checkout screen. Since I had to do something to move forward, I selected the option that came closest to my location. (No, the app didn’t allow freeform text entry of my building or street name). The app again went into a tizzy. When it came back, it displayed the delivery address the way it had reckoned it. This didn’t match my real address.

With so much ambiguity in the delivery address, I wasn’t sure if my order would ever reach me. No sensible customer under those circumstances would pay online by card in advance. Neither did I. I opted for Cash on Delivery.

#2. Delayed Deliveries

Once upon a time, I used to work for a computer hardware manufacturer. The company had two standard payment terms:

- 25% advance, balance 75% against delivery

- 100% advance against 5% cash discount

While the company was otherwise highly ethical in its dealings with its customers, practical cash flow considerations made its managers prioritize deliveries to customers who opted for the first payment term (which is closer to COD) over those who opted for the second payment term (which is closer to online payment).

Looks like ecommerce companies are following the same practice and delaying deliveries to customers who pay online instead of those opting for COD.

Ashish Vyas articulates this problem very well on LinkedIn:

Order a Laptop on 7th April from Flipkart. Expect it to be delivered by 11th April. Delivery partner E-Kart’s phone is not reachable for the entire day on 11th April. The delivery person calls me in the evening to tell me that the delivery couldn’t be done on that day due to manpower shortage and would be done on 12th April 2017, 2.00 p.m. I explain to him that my work is suffering because of the delay in delivery. But he is not bothered and gives me more reasons why he couldn’t deliver on that day. 12th April – Entire day passes, again E-Kart’s telephone is switched off for the whole day. No way I can speak to any executive of Flipkart to understand by when the delivery will be made. Flipkart’s Customer Care only gives an automated response. Now that the money is already with them, they don’t give a damn.

If this guy has learned any lesson from this experience, he’d opt for COD for his next ecommerce purchase.

#3. Fake / Wrong Deliveries

As I’d highlighted in Beware of Credit Card Reward Redemption Theft, fake / wrong delivery of documents, bills and magazines is a widespread problem. Looks like the epidemic is spreading to ecommerce packages now.

@amazonIN your text says package delivered , and here I am waiting for delivery, thank god for COD once again you delivered wrongly

— Chetan Naik (@ChetanDNaik) January 27, 2017

Back in the day, when a courier delivered a consignment, they’d take the customer’s signature on the CCN / POD. That practice has more-or-less gone now. It’s easy for the delivery agent to log a delivery as completed into his app without even visiting the customer’s doorstep. Ergo fake / wrong delivery is rampant, as you can see on this Facebook thread.

If you pay upfront, you’d have to chase the courier. If you opt for COD, the courier will chase you.

Naturally, any sensible human being would like to be chased rather than have to do the chasing.

As the above incidents illustrate, many people who otherwise use credit cards extensively turn to Cash on Delivery when it comes to ecommerce (and, ironically, pay by credit card when they receive the goods at their doorstep!). In each example, the choice of the payment method was dictated more by when than how the payment was made. Contrary to what etailers have been saying, lack of cards etc. didn’t have any role to play in the choice of COD in these cases.

As the above incidents illustrate, many people who otherwise use credit cards extensively turn to Cash on Delivery when it comes to ecommerce (and, ironically, pay by credit card when they receive the goods at their doorstep!). In each example, the choice of the payment method was dictated more by when than how the payment was made. Contrary to what etailers have been saying, lack of cards etc. didn’t have any role to play in the choice of COD in these cases.

This goes back to the raison d’être of COD.

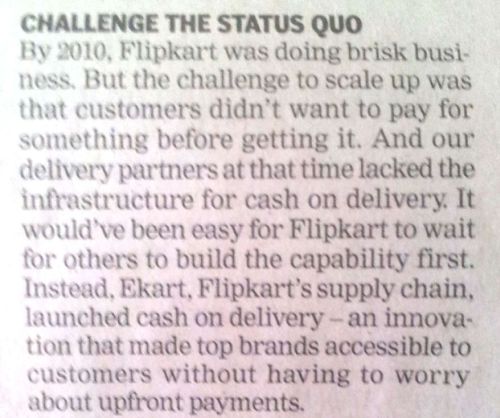

In a recent article in Times of India, Flipkart’s first employee Ambur Iyyappa, spills the beans:

By 2010, Flipkart was doing brisk business. But the challenge to scale up was that customers didn’t want to pay for something before getting it. And our delivery partners at that time lacked the infrastructure for cash on delivery. It would’ve been easy for Flipkart to wait for others to build the capability first. Instead, Ekart, Flipkart’s supply chain, launched cash on delivery.

Ecommerce companies introduced COD to overcome the consumer’s distrust over delivery, which will always take a few days / weeks to happen after placement of the order.

I strongly suspect that it’s the same trust deficit that still drives the popularity of COD for ecommerce in India.

I’m guessing that, over time, banks and fintechs will overcome 2FA-related hurdles to greater use of online payments. But I still suspect that delivery risk will keep COD as the most popular method of payment for Indian online shoppers for a long time to come.

In Will The Sad State Of Logistics Hurt eCommerce?, I’d highlighted the growth challenges posed by core logistics (also called “3PL”) to ecommerce in India. It now appears as if the finance side of logistics (“4PL”) is posing existential threats to the industry. Just when the Flipkarts and Snapdeals of India are trying to turn profits, logistics is pushing their customers to COD (or keeping them there), which is reportedly the costliest method of payment for an online merchant.

UPDATE DATED 12 JULY 2017:

At last, the mainstream media has started reporting what I’ve been saying for years about the real reasons for dominance of COD in India in ecommerce. Apparently, the same is true in the rideshare market as well.

Finally the mainstream media latches on to the real reasons why COD is so high in India despite payment cards being ubiquitous. pic.twitter.com/n80axClNFZ

— GTM360 (@GTM360) July 13, 2017

UPDATE DATED 1 JULY 2018:

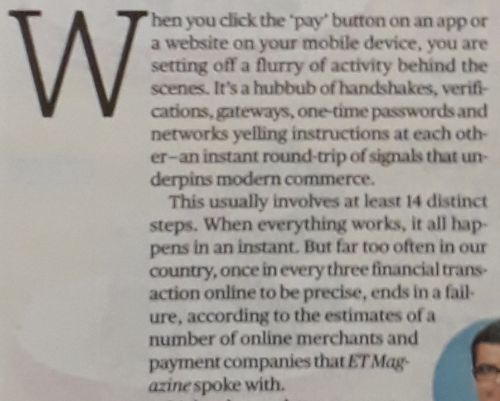

In Exhibit 1 above, I said that there are five moving parts in a 2FA card payment. Looks like I’ve drastically underestimated the number. According to an article in today’s ET SUNDAY, there are 14 distinct steps in a card payment in India.

UPDATE DATED 1 JANUARY 2022:

My wife placed an order on Amazon recently and, as usual, paid online. She didn’t get the delivery for over a month. It took her another 45 days of constant follow to get the refund. She has totally switched to COD now.