In Omnichannel Fiasco #1: Standard Chartered Credit Card, I’d described a recent omnichannel experience that started well but went downhill soon thereafter.

In this post, let me describe another omnichannel experience that was a fiasco from the word go.

This was with Vodafone M-PESA mobile wallet.

When M-Pesa was on the drawing board, my company was invited by Vodafone UK headquarters to bid for developing the solution. Although the MNO subsequently did the work inhouse, my early involvement with M-Pesa piqued my curiosity in the mobile payment service that went on to enjoy cult status in Kenya, where it was first introduced.

Not surprisingly, as soon as the service was launched in India, I was eager to try it out.

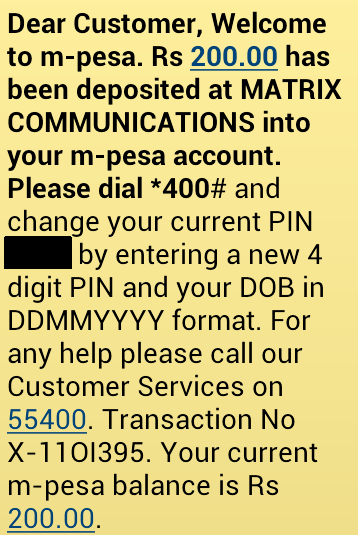

I went to the Vodafone store near my office, filled a form and deposited the minimum amount of INR 200 required to open an M-PESA account. The salesperson at the store warned me that, since the picture on the copy of my identity proof document was slightly smudged, my application might get rejected.

I went to the Vodafone store near my office, filled a form and deposited the minimum amount of INR 200 required to open an M-PESA account. The salesperson at the store warned me that, since the picture on the copy of my identity proof document was slightly smudged, my application might get rejected.

I was relieved when, a few hours later, I received an SMS from Vodafone with a PIN number that I was required to enter into an USSD app to activate my account. When I followed the instructions, the activation failed, with the app displaying a cryptic error message about something called MIME.

Since I couldn’t figure out what the problem with the app was, I went back to the store two days later. The friendly attendant at the store took my phone, dialed up the USSD app, selected an esoteric option that was unrelated to account activation and tapped a few buttons.

Lo and behold, I got an SMS confirming that my account was activated.

I was thrilled that I could now add money into the wallet and pay my bills using M-PESA.

My joy was shortlived.

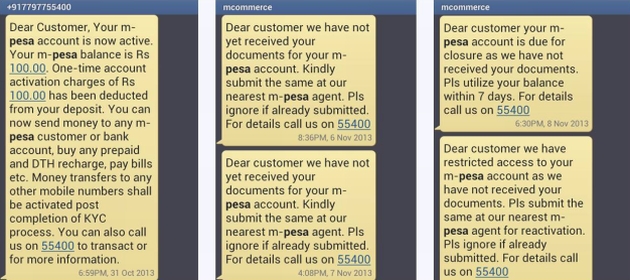

A few days later, I received an SMS asking me to submit the required documentation and, in the same breath, telling me to ignore the message if I had already submitted them.

Not knowing whether to go to the store or ignore the message, I decided to hop channels and called Vodafone’s customer service instead. The CSR confirmed that my account was alive and kicking and told me to ignore the SMS.

However, two days later, I got an SMS saying my account would be closed shortly since I hadn’t submitted the documentation.

I went back to the store, where I was told that 89 out of 105 applications received by the store were rejected on KYC grounds, but that mine wasn’t one of them. So far so good and someone from the store would call me if my application got canned.

Taking me aside, the store manager whispered that his own application was rejected and his account opening amount was blocked. I didn’t know whether to sympathize with him or gloat about being better off than him or both, so I beat a quick retreat from the store.

Several months later, my near-surreal omnichannel experience with M-PESA continues. I still can’t access the money deposited into the wallet. At least it’s much lower than the INR 2000 paid in by the aforementioned manager.